Brandon Bates and Dr. Richard Butler, Department of Economics

Chief executive compensation is a topic of great interest for the general public. Such widespread fascination with the topic likely stems from a predilection for subjects involving extravagance and luxury. Of course, CEO compensation holds an additional dimension of interest for economists. That the CEO does not own the company he runs provides a classic example of the principal agent problem. In this application of the principal agent framework, if the compensation committee were to pay a CEO exclusively with a base salary, the executive would have an incentive to shirk or maintain the status quo. Offering a mixture of base salary and performance pay gives the chief executive officer a vested interest in company performance.

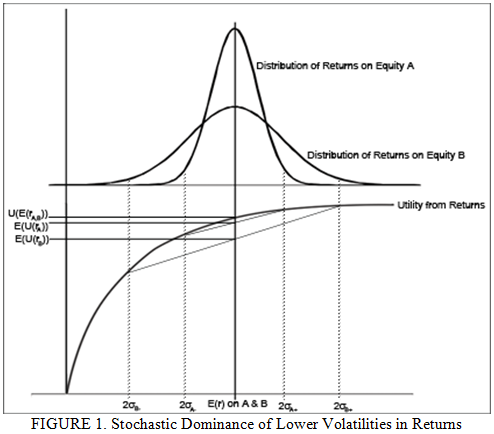

Due to diminishing marginal benefit of wealth, CEOs of companies with more volatile stock prices will have lower expected benefits of wealth. As such, we expect to see CEOs in industries with volatile stock prices receiving fewer stock awards as a percent of total compensation than CEOs in an industries marked by more stable stock prices, ceteris paribus. Figure 1 illustrates this concept. Distributions a and b are normally distributed, differing only in their variances. While they both have the same expected return, distribution a has a higher E(U(r)) (expected happiness from wealth) than b. Hence, distribution a stochastically dominates b.

Several studies have shown an empirical relationship between equity risk and performance pay, but in the treatment of the subject, these papers confine their investigations to connections involving total equity risk. None of the studies decomposes total risk into its components – viz., idiosyncratic and market risk. Although the theoretical principal agent framework suggests that the compensation committee should tie performance incentives to firm-specific risk, without separating total risk into its components it is unclear whether idiosyncratic risk, unsystematic risk, or a mixture of the two drives the demonstrable empirical relationship.

Inasmuch as managers have control over firm performance, neither the idiosyncratic risk nor the manager’s income lottery due to this risk is fully randomized. Market risk and its concomitant income lottery are, however, unaffected by managerial decisions and are, from the executives’ perspective, fully stochastic. As such, we expect to see a negative relation between market risk and compensation given in stock awards. It is this relationship that I show to exist.

To investigate the role of market risk, we need a measure of variability in stock returns that assumes away all idiosyncratic risk. The beta slope coefficient from the Capital Asset Pricing Model (CAPM) assumes a well-diversified portfolio in its derivation – such an assumption eliminates all idiosyncratic risk. By using beta as a proxy for market risk, I employ a measure addressing only the risk over which the CEO has no control – the risk associated with market movements. In doing so, I create true income lottery.

In the estimation of the empirical relationship between beta and the percent of total compensation taken in stock awards, I use an instrumental variable estimation technique called three stage least squares (3SLS). As posited, the percent of total compensation in stock awards is negatively related to the firm’s beta. In fact, in my sample, every unit increase in the beta results in a 13.46% decrease in the percentage of compensation taken in stock awards. This result is both strong and statistically significant. This is surprising as most industry practitioners view the compensation decisions as completely decoupled from market risk considerations.

The findings of this paper have been well received. Many interested researchers have sent inquiries since I posted it on the SSRN, and I have been informed of its citation in other papers. Additionally, the Midwest Economics Association accepted this paper for presentation at its annual conference in Chicago next March. All presented papers are published in the conference proceedings.

This paper extends our understanding of the role risk aversion plays in executive compensation packages by demonstrating a marked relationship between market risk and levels of stock awards. Additionally, my approach to this topic implicitly posits a new consideration when studying the effects of equity risk on compensation structures. Videlicet, researchers should contemplate separating total risk into its systematic and unsystematic components. Certainly, the discussion of the principal agent problem is not finished. On the contrary, it continues to

gain prominence as fresh perspectives and theories emerge. If nothing else, the natural curiosity about excesses will keep the research moving forward.