Bryan Graden and Dr. Ted Christensen, School of Accountancy

In addition to mandatory disclosures such as SEC filings, managers have the option of disclosing information voluntarily to the public. Press releases and conference calls are two ways managers often reveal information to the market, and one of the most important disclosures made through these venues is the forecast of future earnings. Prior research has found that investors rely on information received from management earnings forecasts (MEFs). Since managers are involved in the day-to-day activities of their companies, they have access to important “insider information.” As a result, investors rely heavily on this information in forming expectations about the company. Therefore, it isn’t surprising that prior research documents that MEFs often affect stock prices. While prior research has explored the extent to which MEFs influence investors’ decisions, it has not thoroughly investigated when and why managers choose to issue MEFs. The focus of this project is to explore factors associated with managers’ decision to forecast earnings in a given year.

Prior research has explored manager motivations for issuing forecasts in connection with bad news, equity offerings, and when information asymmetry is high. This study takes a more general approach, combining these and other factors into one predictive model. I use a logit model to make predictions about when managers will issue earnings forecasts. In order to estimate the model, I collected data for years in which managers choose to disclose an earnings forecast as well as years in which they do not issue a forecast. I used SAS to extract company financial data from the Compustat database and constructed variables for my predictive model, such as price and earnings volatility. The following equation represents my model for predicting whether management will issue an annual earnings forecast:

FORECAST = β0 + β1PRIOR_YEAR + β2FN +β3EPS + β4DEBT_EQUITY + β5PRICE_VOL + β6EARNINGS_VOL + β7DECREASE_EPS + β8LOSS + β9LOG_TASSETS + β10-18(SIC0-SIC9) + ε

Where:

FORECAST=indicator variable coded one if management issued an annual earnings forecast and zero otherwise,

PRIOR_YEAR=indicator variable coded one if managers forecasted earnings in the prior year and zero otherwise,

FN=forecast news measured as the difference between management’s forecast and analyst expectations,

EPS= current company performance measured as annual earnings per share,

DEBT_EQUITY = company leverage measures as total liabilities divided by total equity,

PRICE_VOL = price volatility calculated as the standard deviation of quarterly price over the past eight quarters,

EARNINGS_VOL = earnings volatility measured as the standard deviation of quarter EPS over the past eight quarters,

DECREASE_EPS = indicator variable coded one if EPS decreased during the period of the forecast and zero otherwise,

LOSS = indicator variable coded one if the company incurred a loss (i.e., EPS < 0) and zero otherwise,

LOG_TASSETS = control for firm size,

SIC1-SIC9 = industry indicator variables to control for systematic differences across industries.

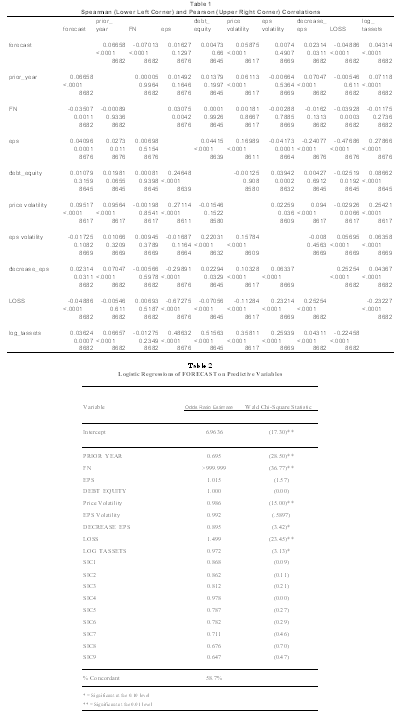

Table 1 presents pairwise correlations among the major variables in the model. The top row and first column present univariate tests of the hypothesized relations between each of the key predictor variables and managers’ propensity to issue forecasts (FORECAST). The results indicate that managers are more likely to issue an earnings forecast if (1) they issued a forecast last year, (2) they expect to fall short of analysts’ forecasts, (3) earnings performance is strong, (4) stock price is volatile and subject to severe drops, (5) earnings are less volatile (and presumably easier to forecast), (6) earnings are expected to go down from the previous year, (7) a profit is expected for the period.

Table 2 summarizes the results of the logit model. The benefit of this analysis is that it explores the relations discussed in Table 1 in a multivariate context. Thus, Table 2 allows the investigation of the association between each of these variables and the decision to issue a forecast while simultaneously controlling for the effects of the other predictor variables, firm size, and systematic differences across industries. The estimated odds ratio estimates indicate that firms are more likely to issue MEF when (1) they issued a forecast last year, (2) they expect to beat analysts’ forecasts, (3) stock price is volatile and subject to severe drops, (4) earnings are expected to go down from the previous year, (5) a loss is expected for the period. These results are not completely consistent with the univariate results, presumably because pairwise correlations do not control for the effects of other variables.

The model correctly classifies firms about 59% of the time. Thus, while the model identifies some factors that are significant predictors of firms’ decision to issue MEFs, future research can improve the explanatory power of the model. Increasing the sample size and including more variables such as firm-specific risk or industry risk could help to increase the predictive ability of the model. These results will be useful for investors and researchers in predicting when management will forecast earnings.