Daniel Sullivan and Dr. Frank McIntyre, Economics

Main Text

Past research has documented a wide array of personal risk factors for declaring bankruptcy, such as a loss of income, medical debt, excessive credit card debt, and large mortgages. These factors fall into two broad categories: adverse events, such as an acute income shock (e.g., job loss), and internal decisions, like budgeting failures where a household’s consumption exceeds income for some time.

One problem with prior research on these topics is that adverse income shocks are calculated using data from only the two years prior to filing, making long-term income events unobservable. One set of commonly used survey data shows that households rarely file for bankruptcy in haste, often weighing the decision for months or years. Thus households may experience relevant income shocks years before filing. Furthermore, it is very difficult to know if a debt burden listed on a household’s filing is due to a long-term budgeting failure without being able to observe the long-term consumption decisions of the household.

This project closes this research gap by using the Panel Study of Income Dynamics (PSID) to recover the long-term income and consumption profile of the bankrupt for ten years before and after filing for bankruptcy. In all cases, a group of households with the same demographic characteristics as the bankrupt is used for comparison and is followed over an equivalent 21-year span. We find that while a typical household’s income trends upward over the long term, this is not true for the bankrupt, who typically see their income stagnate and decline slightly. This may conflict with expectations they base on their non-bankrupt peers’ experiences.

We then turn to the question of consumption. We use the PSID data on consumption to demonstrate that for both the comparison group and bankrupt households, consumption increases over time. However, even ten years before filing, bankrupt households are consuming at levels more congruent with higher-income households. This consumption imbalance grows worse as they continue to emulate their peers’ increasing consumption despite their own faltering income.

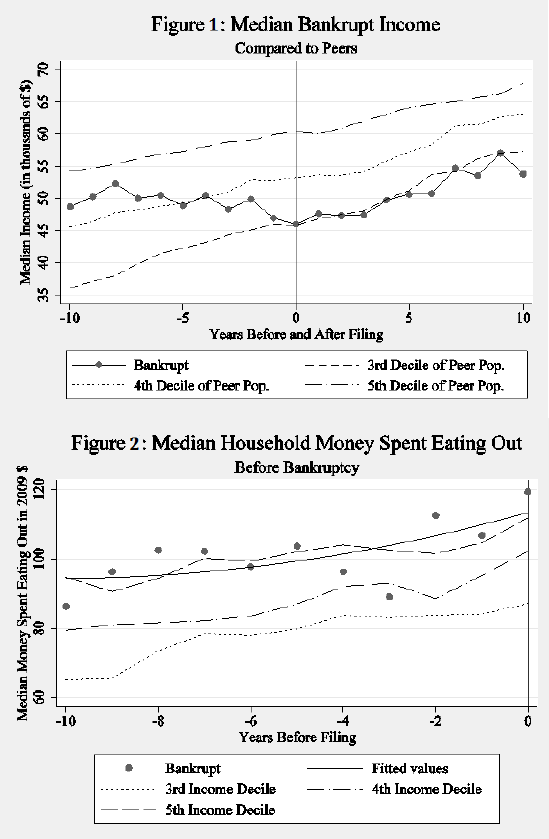

In order to accurately compare the bankrupt and non-bankrupt, we reweight the non-bankrupt population to match the age, education, and year profiles of the bankrupt. Figure 1 depicts the income stream of the bankrupt for 10 years before and after filing and the equivalent time period for the non-bankrupt. The non-bankrupt sample is divided by their income in the starting year (year -10) and the 3rd, 4th, and 5th deciles of the income distribution are depicted. As Figure 1 shows, 10 years before bankruptcy, the median bankrupt income is between the 4th and 5th income deciles. Over the next ten years, however, the non-bankrupt experience income growth characteristic of a normal life-time earnings pattern, while the bankrupt see little growth or even slightly negative growth. It is possible that the bankrupt, not knowing they are destined for bankruptcy, engage in consumption similar to their peers while expecting their income to catch up to their peers in the near future. In this hypothetical situation, the median bankrupt household accumulates roughly $50,000 in debt, much more than the average debt at time of filing. This is, of course, hypothetical. Figure 3 provides evidence that the bankrupt do, in fact, consume like their non-bankrupt peers. Specifically, it shows yearly expenditures on food outside the home, a reasonable measure of discretionary spending for a household, in the same way income is depicted in Figure 1.

From Figures 1 and 3, we see that the while the median incomes of the bankrupt and the 5th decile non-bankrupt diverge more and more over time, with a yearly difference of almost $10,000 at the time of filing, the consumption behavior of the bankrupt follows that of the non-bankrupt. Other consumption measures, such as home equity, and total expenditures on food and housing show similar patterns. (Unfortunately, only a fraction of our results can be presented here. The interested reader can find the full text of “Long-term Income Stagnation among the Bankrupt” at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1684616). These results undermine the adverse events hypothesis and support the internal decisions, or strategic hypothesis. My adviser and I are currently preparing the fully developed paper for submission to an economic journal.

References

- The internal decisions hypothesis includes a number of other behaviors, like using bankruptcy strategically. For simplicity, I focus on the commonly thought of motive for bankruptcy, long-term budgeting failure.

- Mann, R.J. and K. Porter. 2010. “Saving Up for Bankruptcy.” The Georgetown Law Journal 98, pp. 289-339.