Jonathan Holloway and Dr. James C. Brau, Department of Finance

Background

Overall, three phenomena exist in corporate equity issuances. These phenomena include hotissue markets, first-day underpricing, and poor long-run performance. Hot-issue markets refer to fluctuation in the volume of issuances. Hot waves are periods of high issuance volume, and cold waves are periods of low volume. The second phenomenon, first-day underpricing, results in the initial price of equity beginning lower than its first-day closing price. The third phenomenon, poor long-run performance, refers to the tendency of issuances to underperform during a period beginning the day after the issuance and ranging from one to five years.

Study Description

In this study, Dr. Brau and I examined the key equity issuance phenomena of hot-issue markets, first-day underpricing, and poor long-run performance as they relate to the healthcare industry. The research and findings applied specifically to the healthcare industry are of interest due to the lack of extant healthcare research and the unique nature of the industry. As explained by Guirguis, Onochie, and Rosen (2001)1, healthcare differs significantly from other industries due to the influence of nonmarket forces related to government policy.

Hypothesis

We hypothesized that trends in the healthcare markets would be similar to those of the phenomena found in the overall markets. Thus, we hypothesized that hot-issue markets would exist. We also hypothesized that initial underpricing and long-run underperformance would occur among healthcare initial public offerings (IPOs) and later offerings known as seasoned equity offerings (SEOs). Finally, we expected negative sales growth over the same period for long-run performance among both types of offerings.

Conclusion

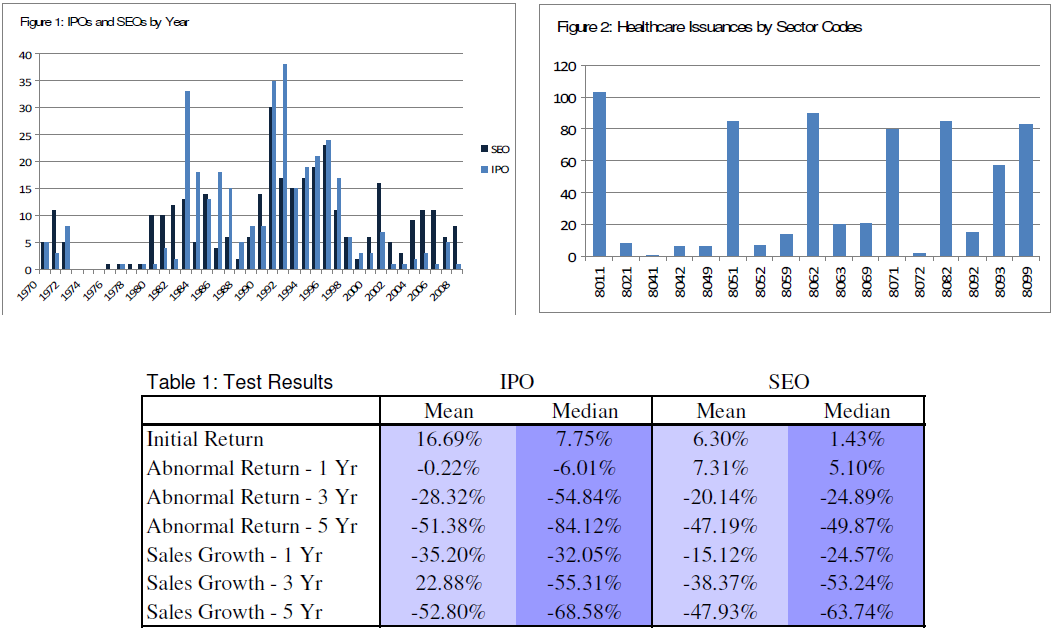

Hot-Issue Markets: From our analysis, we found hot-issue markets existed in healthcare IPOs and SEOs as shown in Figure 1. Not only did hot-issue markets exist, but Figure 2 demonstrates that six of the 17 healthcare sectors accounted for 76.02% of the industry’s IPOs and SEOs from 1970 to 2008.

Initial Underpricing: As hypothesized, we also found that IPOs experienced a mean (median) underpricing of 16.69% (7.75%) while SEOs were less underpriced at 6.30% (1.43%). Table 1 depicts these findings and those of the longrun price performance and sales growth.

Long-run Performance: In the case of abnormal returns, both IPOs and SEOs experienced long-run underperformance with the exception of one-year abnormal SEO returns. For IPOs, one-, three-, and five-year returns underperformed by a mean (median) of –0.22% (–6.01%), –28.32% (–54.84%), and –51.38% (–84.12%), respectively. For SEOs, the same measures were 7.31% (5.10%), –20.14% (–24.89%), and –47.19% (–49.87%).

Similarly, sales growth was negative for IPOs and SEOs over the same periods with the exception of the three-year mean IPO sales growth. The mean (median) sales growth for IPOs over one-, three-, and fiveyear periods was –35.20% (–32.05%), 22.88% (–55.31%), and –52.80% (–68.58%), respectively. The same periods for SEOs included mean (median) growth rates of –15.12% (–24.57%), –38.37% (– 53.25%), and –47.93% (–63.74%).

Of our findings, only one-year abnormal returns and three-year sales growth figures for IPOs failed to have statistical significance. The results indicate that all three of the new issuance phenomena will likely exist in the healthcare industry and that further attention should be given to each. We intend to publish this study in the Journal of Health Care Finance or a similar venue.