David Beheshti and Richard Evans, Economics

Introduction

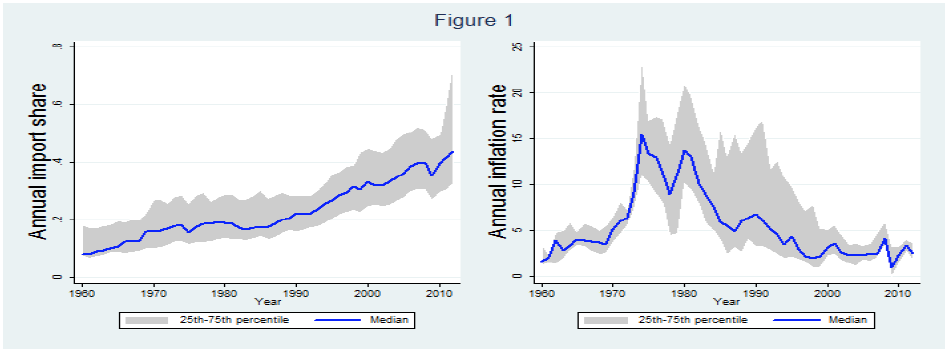

Since the collapse of the Bretton-Woods Agreement in 1973, inflation rates have been steadily decreasing in most of the developed world. At the same time, countries have become increasingly open to international trade (see Figure 1). A possible explanation is that openness to trade and inflation are negatively correlated. This relationship is predicted in a highly-cited theoretical model by economist Kenneth Rogoff (1985) and in most of the previous literature on the subject. However, a more recent theoretical paper (Evans 2012) predicts that countries may engage in inflationary policy in order to tax foreign holders of domestic currency. As countries increase in openness, the inflation tax becomes an increasingly attractive option. Critical to this insight is the level of imperfect competition within the country, as imperfect competition dampens the incentive of central banks to inflate. Knowing the extent to which countries actually use this inflation tax has important policy implications. For example, if countries regularly engage in this practice then other countries may be hesitant to hold foreign currencies, which could cause inefficiencies in international trade.

The two theories differ in that Rogoff’s theory, which predicts a negative relationship between openness and inflation, assumes that monetary authorities act with discretion, while Evans’ theory assumes that monetary authorities commit to a policy rule and then follow that rule. While the former may have been an accurate characterization of monetary policy twenty years ago, most countries have moved toward following monetary policy rules. However, monetary authorities may still use discretion in order to respond to short-run economic fluctuations.

Our research shows the two different theoretical models are both correct, but describe somewhat different aspects of monetary policy, one describing the short-run effects of openness and the other the long-run effects.

Methodology

In order to test the validity of these two theoretical models, we ran two different empirical tests. The first was a simple fixed-effects panel regression to estimate the relationship between openness and inflation while controlling for the level of imperfect competition. We also included per capital gross domestic product (GDP) as a proxy for the level of development and the rate of central banker turnover as a proxy for commitment to a policy rule. Openness was measured as the ratio of imports to GDP. We used two alternative measures to estimate the level of imperfect competition within each country. The first was an estimate of the average markup of price over marginal cost. Data on markups was not readily available, so we developed our own estimates following the method of Roeger (1995) and Martins et al. (1996). Unionization, our other proxy for the level of imperfect competition, was computed as the number of active trade union members divided by the number of wage and salary earners. Our main data source was the Organisation for Economic Co-operation and Development (OECD). Not surprisingly, many of these time series were nonstationary, so we created detrended versions of all the nonstationary series. Our regressions specification was then ![]() where Φ is the country fixed-effects.

where Φ is the country fixed-effects.

Our second test was to run a cross-sectional regression. Romer (1993) demonstrated a very robust negative relationship between openness and inflation, and his paper is the reference point for most subsequent empirical papers on the topic. We begin with a specification similar to that of Romer but with one key difference. As previously mentioned, the data are not stationary. Openness and per capita GDP both have a clear upward trend, while inflation has a clear downward trend. This nonstationarity biases the regression results from an ordinary least squares regression. To correct for this, we define all nonstationary variables as the average growth rate over the relevant time period.

Results

Our main contribution to the empirical literature comes from our cross-sectional regressions. In sharp contrast to most of the previous literature, we obtained regression coefficients for openness that are positive and statistically significant at the five percent level. Our panel regressions, however, seem to confirm the findings of Romer. In almost every model specification, the coefficient of openness is either negative or statistically insignificant.

Discussion and Conclusion

The differing results from our panel and cross-sectional regressions can be explained by differences in the assumptions of the theoretical papers by Rogoff and Evans. Since monetary authorities often use discretion in response to short-run economic fluctuations, it is not surprising that we obtained negative coefficients in our panel regressions, which capture more of the short-run effects. Our cross-sectional regressions, which capture more of the long-run effects, show a positive relationship. This is consistent with central banks adherence to a policy rule in the long-run. Thus we argue that both theoretical models are correct, but describe different aspects of monetary policy, which can be seen from the different assumptions of the respective models. Our main result is that openness can be inflationary.